Services to the rescue?

A sharp fall in the global manufacturing PMI new orders index in July confirms renewed industrial weakness. The companion services survey, however, reported an uptick in the new business component, which is close to its post-GFC average. Will services resilience sustain respectable overall growth?

The understanding here is that economic fluctuations originate in the goods sector, reflecting cycles in three components of investment – stockbuilding, business fixed capex and housing. Multiplier effects transmit these fluctuations to the services sector – there is no independent services cycle.

The manufacturing new orders and services new business indices have been strongly correlated historically, with Granger-causality tests indicating that the former leads the latter but not vice versa*.

Several considerations suggest that the recent divergence will be resolved by the services new business index moving lower:

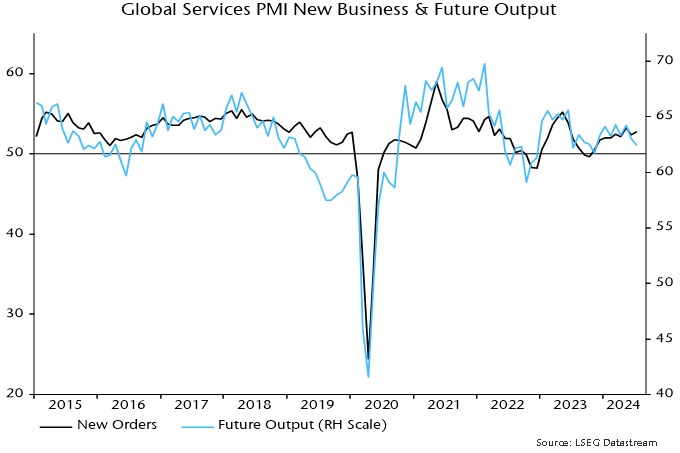

1. The services future output index correlates with new business and fell to an eight-month low in July – see chart 1.

Chart 1

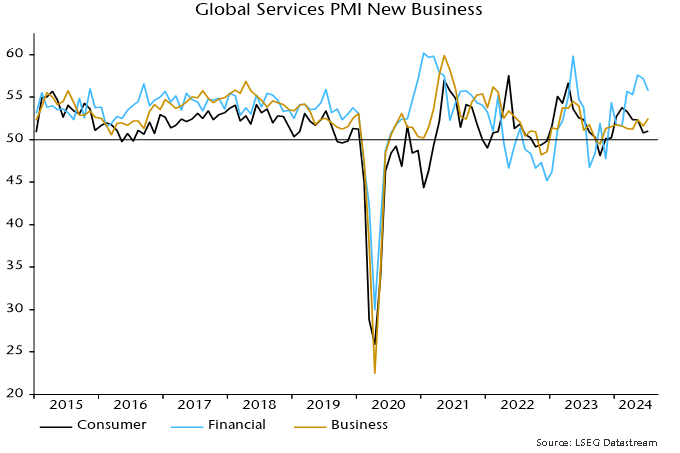

2. Recent new business readings have been inflated by strength in financial services – chart 2. Financial services new business correlates with stock market movements, suggesting weakness ahead.

Chart 2

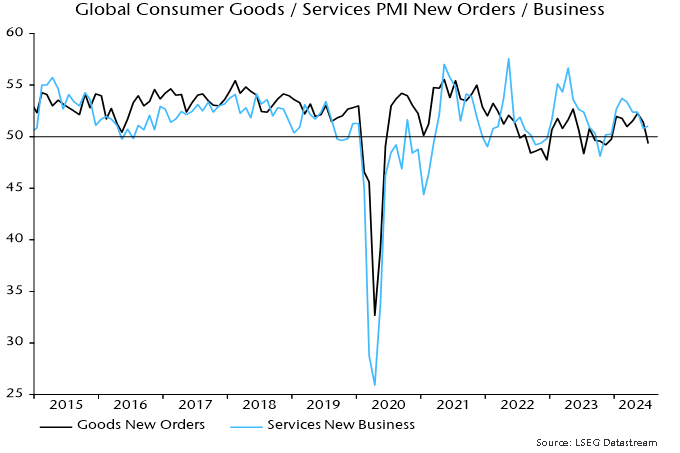

3. Consumer services new business correlates with the manufacturing consumer goods new orders index, which fell below 50 in July – chart 3.

Chart 3

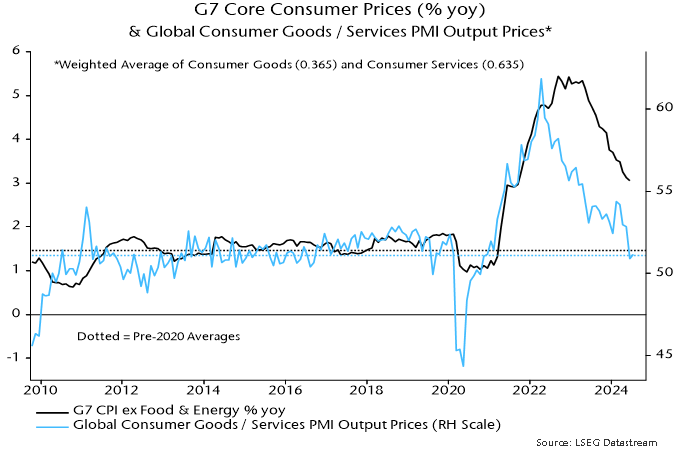

Output price indices for consumer goods and services support the optimism here about inflation prospects through mid-2025. A weighted average has fallen back to its October 2009-December 2019 average, a period in which G7 annual CPI inflation excluding food / energy averaged 1.5% – chart 4.

Chart 4

*Contemporaneous correlation coefficient since 1998 = +0.84. Granger-causality tests included six lags. Manufacturing terms were significant in the services equation but not vice versa.