Money Moves Markets

Will Truss largesse reverse dangerously weak UK money trends?

September 7, 2022 by Simon Ward

UK monetary trends continue to argue against Bank of England policy tightening.

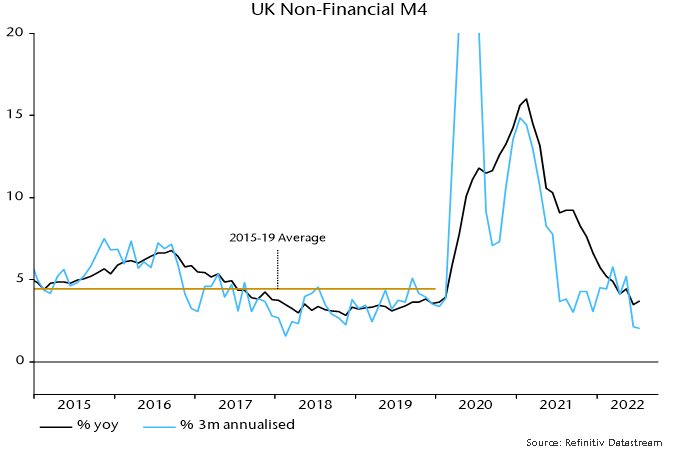

Annual growth of non-financial M4 – comprising money holdings of households and private non-financial firms – was 3.7% in July, below a 4.4% average in the five years preceding the pandemic. The aggregate expanded at an annualised rate of only 2.0% in the latest three months – see chart 1.

Chart 1

Growth of the Bank’s preferred broad money measure, M4ex, is higher, at 4.8% in the year to July and 4.9% annualised in the latest three months. This aggregate includes money holdings of financial companies, which have been rising strongly but are of little relevance for near-term demand prospects.

Excessive money growth in 2020-21 boosted demand and “accommodated” price pressures due to various supply shocks, resulting in current high inflation. Is there still a monetary overhang from that period, warranting further policy tightening despite recent slow money growth?

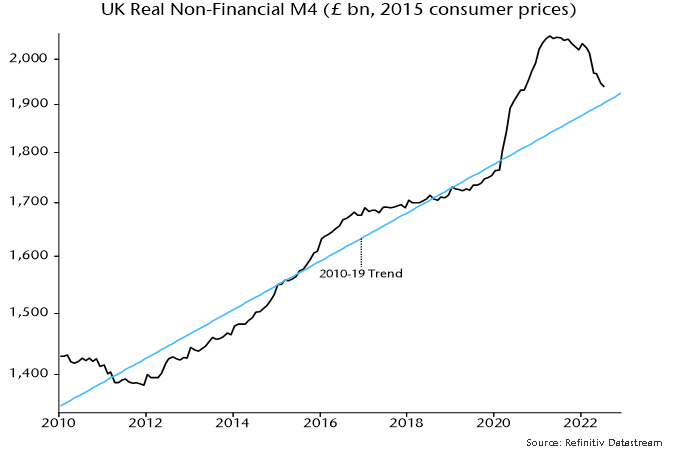

Expressed in real terms relative to consumer prices, non-financial M4 is almost back to its pre-pandemic trend – chart 2. The suggestion is that the monetary excess has already been largely “absorbed” by higher prices.

Chart 2

In the absence of an overhang, the recent pace of money growth, if sustained, should be consistent with inflation returning to target within the two to three year horizon relevant for policy. Further tightening risks unnecessary economic pain and an eventual undershoot.

Are the Truss government’s plans for large-scale fiscal loosening inflationary, warranting offsetting monetary policy action?

Whether energy subsidies, tax cuts etc. will prove inflationary depends on how they are financed. The banking system is likely to provide at least part of the funding, implying a first-round boost to broad money.

A renewed rise in annual non-financial M4 growth to more than 6% would be inconsistent with medium-term inflation normalisation, requiring offsetting Bank action.

Such a scenario, however, is far from guaranteed. Money growth was arguably on course to fall to a dangerously low level, reflecting planned Bank QT of £80 billion a year (equivalent to 3.4% of the current level of non-financial M4), a slowdown in mortgage lending and external outflows due to an expanded balance of payments deficit.

A boost from monetary financing of fiscal loosening may offset such negative influences without pushing money growth significantly higher.

A sensible approach, therefore, would be for the Bank to wait to assess the monetary consequences before deciding whether fiscal plans require a policy response. The current MPC membership, of course, has no understanding of or interest in monetary analysis.

The Keynesian consensus view is that fiscal expansion necessarily implies a higher level of demand that the Bank cannot allow. The monetarist response is that, unless it leads to faster money growth, fiscal loosening will push up market interest rates and “crowd out” private spending. Surging gilt yields suggest that this scenario is already playing out. The Bank should avoid piling on the pain.