Money Moves Markets

US broad money still growing too fast

December 15, 2021

US core consumer price momentum is likely to slow sharply in early 2022 but monetary trends appear inconsistent with inflation returning to its pre-pandemic level.

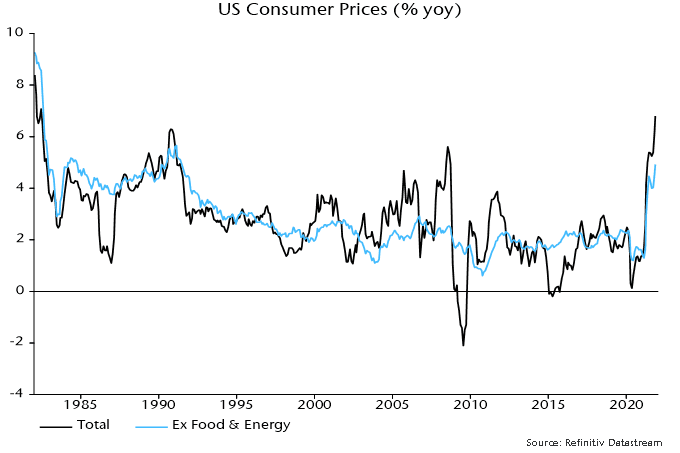

Headline and core (i.e. ex. food and energy) annual inflation rates rose to their highest levels since 1982 and 1991 respectively in November (6.8% and 4.9%) – see chart 1.

Chart 1

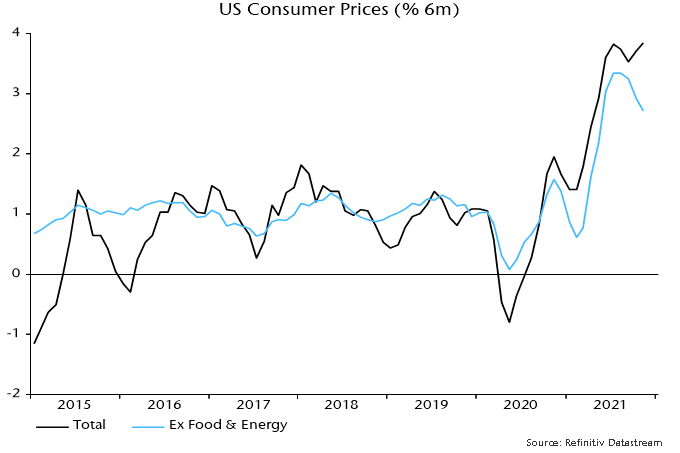

On a six-month rate of change basis, however, core momentum eased for a third month, albeit remaining high at 2.7% or 5.5% annualised – chart 2. Headline momentum was boosted by a further acceleration of food prices.

Chart 2

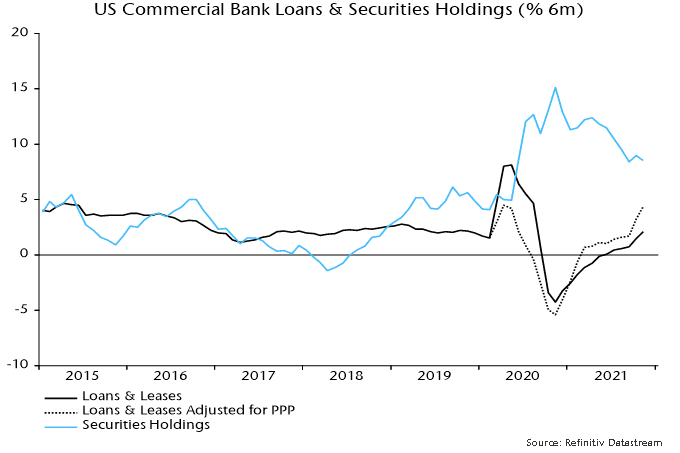

The moderation in core momentum mirrors a slowdown in six-month growth of broad money 14 months earlier – chart 3. The apparent relationship suggests a further significant fall in six-month core inflation.

Chart 3

A 14-month lead is notably shorter than the average in historical studies of the relationship between money and prices. The judgement here is that supply disruption due to the pandemic has accelerated the transmission mechanism.

While core momentum could slow faster than expected in early 2022, broad money trends argue against a return to the pre-pandemic level: core inflation averaged 2.0% over 2015-19. Six-month growth of the broad measure calculated here* is running at an annualised rate of about 9% versus a 2015-19 average of 5%.

Broad money growth is being boosted by strong expansion of commercial bank assets as well as ongoing QE. Adjusting for PPP loan forgiveness, banks’ lending book grew by about 9% annualised in the six months to November, with securities holdings rising by 18% – chart 4.

Chart 4

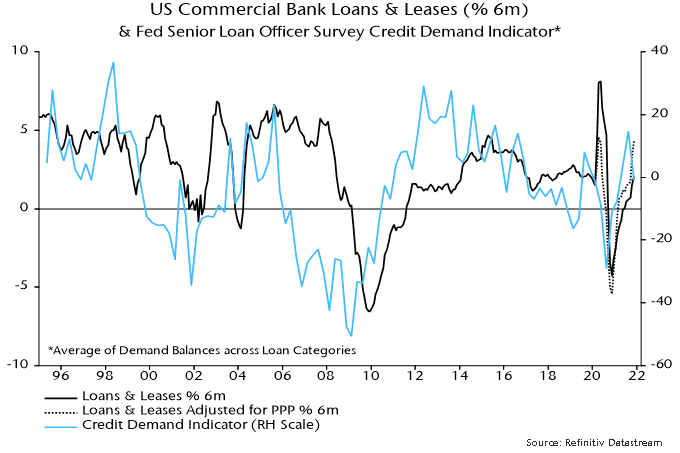

Banks are well capitalised and highly liquid but the October Fed loan officer survey suggested a cooling of credit demand – chart 5. Securities purchases, meanwhile, could slow as QE tapering and a rebound in the Treasury’s cash balance at the Fed following Congressional approval of a rise in the debt ceiling relieve upward pressure on bank reserves.

Chart 5

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.