Money Moves Markets

UK MPC inaction risks sterling inflation boost

November 5, 2021 by Simon Ward

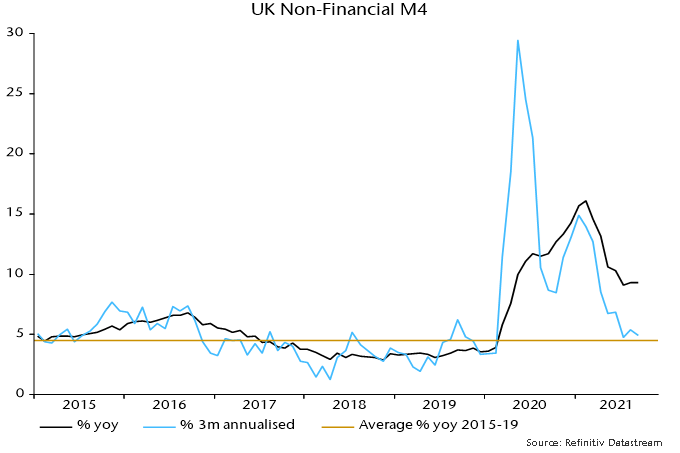

Bank of England Governor Andrew Bailey is under fire for miscommunication in the run-up to this week’s MPC meeting. A much bigger error was the Committee’s decision a year ago to boost QE by a further £150 billion at a time when annual broad money growth – as measured by non-financial M4 – was running at 11.7%.

The extra QE contributed to annual money growth rising further to a peak of 16.1% in February 2021, with the additional monetary excess to be reflected in a higher inflation peak in 2022 and a slower subsequent decline than would otherwise have occurred.

So should the MPC have hiked this week? Annual non-financial M4 growth was still 9.3% in September but the three-month pace of expansion has moderated to an annualised 4.9%, not far above a 2015-19 average of 4.5% – see chart 1.

Chart 1

The view here has been that the MPC should move rates back to 0.5-0.75% to reinforce the recent monetary slowdown and then wait for guidance from the numbers. Sustained sub-5% expansion would be consistent with (core) inflation returning to target, though probably not before H2 2023.

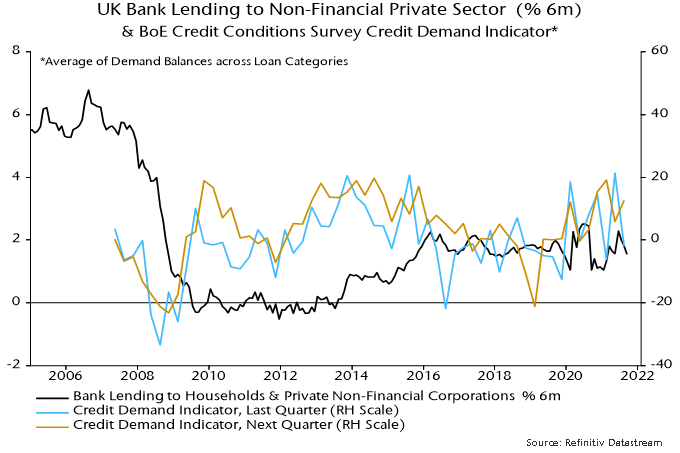

Higher rates would be needed in the event of a credit-driven rebound in money growth. Bank lending expansion has weakened recently, partly reflecting the ending of the stamp duty holiday, but expected loan demand balances mostly improved in the latest Bank of England credit conditions survey – chart 2.

Chart 2

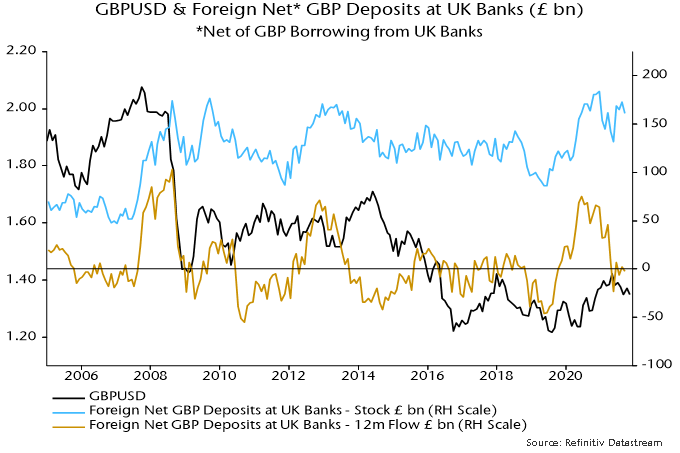

The MPC’s miscommunication / delay risks triggering a fall in sterling, which would magnify near-term inflation difficulties. The exchange rate appears to have been boosted in 2019-20 by overseas investors increasing their net sterling deposits at UK banks – chart 3. These inflows stopped in 2021 but a large stock position could be liquidated if investors lose faith in UK policy-making.

Chart 3