Money Moves Markets

UK inflation still reflecting 2020-21 monetary strength

March 22, 2023 by Simon Ward

Current monetary stagnation implies that policy-makers’ worries about a sustained inflation overshoot are as misplaced as their deflation panic in 2020 when money growth was surging.

UK annual broad money growth peaked in February 2021. It should be no surprise that annual inflation was still riding high in February 2023, based on the “monetarist” understanding of a roughly two year lead.

Annual money growth, however, collapsed after February 2021. Non-financial M4 rose by 2.4% in the year to January and by only 0.9% annualised in the latest three months.

A consensus concern is that a coming inflation decline will fail to return it to target – one informed commentator expects stickiness at about 4%. No explanation is offered of how such a scenario is compatible with barely growing broad money. Is velocity expected to pick up, against its long-term downtrend? Or is 4% inflation projected to coexist with economic contraction of 3% pa – the implication if money growth runs at 1% pa and velocity is stable?

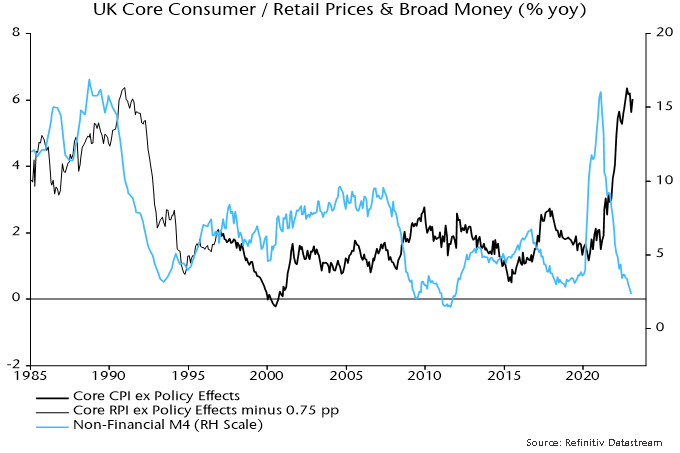

The collapse in annual money growth closely resembles a decline over 1990-93, following which annual core RPI inflation fell below 2% in H2 1994, consistent with a core CPI rate (unavailable then) of about 1% – see chart 1.

Chart 1

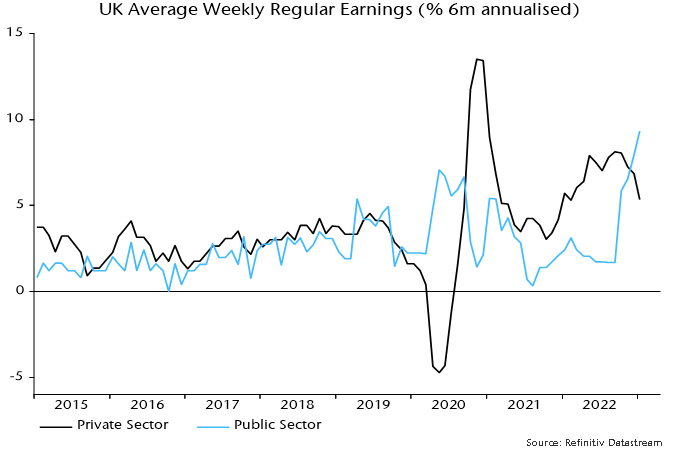

The push-back to a similar scenario now is that the unemployment rate is much lower than at the start of the 1990-92 recession. Average earnings growth, however, was significantly higher then – the annual increase in total pay was above 10% (three-month moving average) when the recession started versus below 6% now. Private pay momentum is already slowing despite limited labour market cooling to date – chart 2.

Chart 2

The 1991-1994 inflation plunge, moreover, occurred despite upward pressure on import prices from a 12% drop in the effective exchange rate between 1990 and 1993 (calendar year averages). There is no such currency headwind to an inflation decline now.

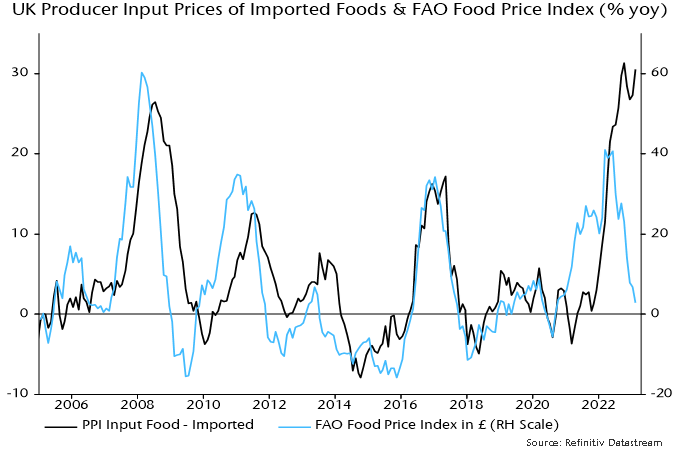

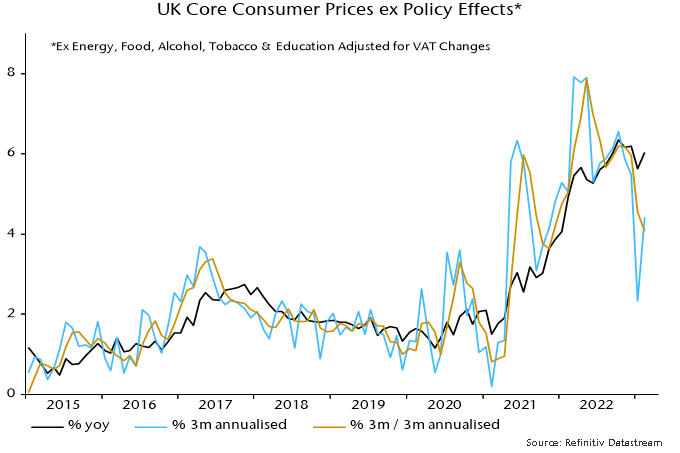

Annual core CPI inflation rose in February but three-month momentum remains well down from its May 2022 peak – chart 3. Commodity prices signal a coming slowdown in food inflation – chart 4 – while energy prices will soon be falling year-on-year. The February inflation result is irrelevant for assessing 2024-25 prospects and the MPC should ignore it.

Chart 3

Chart 4