Money Moves Markets

UK inflation forecast update: still on track for 3%+

May 25, 2021 by Simon Ward

A post in November presented a “monetarist” forecast that CPI inflation would rise to more than 3% by late 2021. This forecast appears on track.

The Bank of England’s central projection for Q4 2021 was 2.1% in November. This was lowered to 1.9% in February but raised to 2.5% in May.

A key element of the November forecast was a significant inflation boost from energy prices, reflecting a view that a strong global industrial recovery would push up oil and other commodity prices. This has played out: the CPI energy component rose by 7.5% in the year to April, contributing 0.5 percentage points (pp) to annual CPI inflation of 1.5%.

The energy effect explains the upward revision to the Bank of England’s forecast. The Bank now expects the contribution of energy prices to annual inflation to rise further to 0.75 pp by Q4 – similar to the view here, which assumes an additional 5% increase in the Ofgem price cap in October.

The forecast that CPI inflation will exceed 3% by year-end is driven by three additional factors:

- The planned increase in VAT in the hospitality and tourism sectors from 5% to 12.5% in October, with a return to 20% scheduled for April 2022.

- A pick-up in food price inflation, partly reflecting recent strength in global food commodity prices.

- A rise in underlying core inflation (i.e. excluding the VAT effect as well as energy / food contributions) in lagged response to faster broad money growth.

Taking these in turn, the forecast assumes that there will be 35% pass-through of the VAT rise to prices, implying a 0.2 pp boost to the monthly change in the CPI in October. The Bank and consensus, by contrast, appear to assume a negligible impact. This is surprising: firms face rising costs and the withdrawal of government support while economic reopening should ensure strong demand – why would they allow margins to take the full hit from the VAT hike?

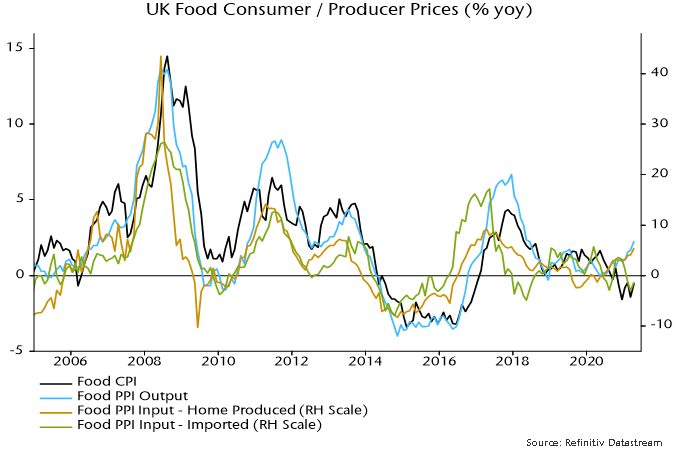

Food prices have so far been weaker than assumed in the November forecast here, falling by 0.5% in the year to April. Producer output prices of food products, however, were up by 2.3% over the same period, the largest annual rise since 2018 – see chart 1.

Chart 1

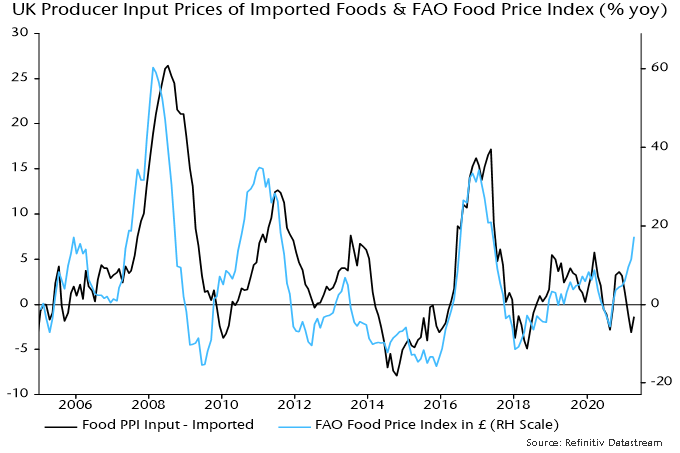

The pick-up in producer output prices appears to have been driven by higher input costs of home-produced food. Imported food materials, by contrast, have cheapened, partly reflecting sterling appreciation. This is about to change: the FAO global food commodity price index rose by 17% in sterling terms in the year to April – chart 2.

Chart 2

The forecast here continues to assume that annual CPI food inflation will rise to 2.0% by December.

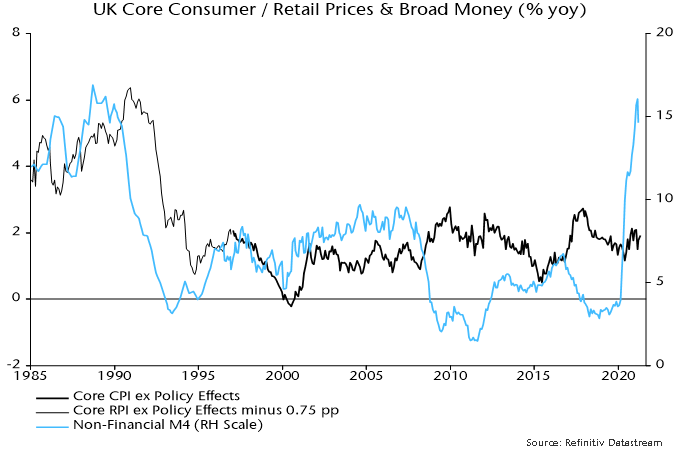

The final element of the forecast is an expected further rise in underlying core CPI inflation. Actual core inflation (i.e. excluding energy, food, alcohol and tobacco) was 1.3% in April but the assumption of 35% pass-through of the VAT cut in hospitality and tourism implies a significantly higher underlying rate, of 1.9%. The underlying rate has risen from a low of 1.2% in May 2020.

Research previously reported here found a consistent directional leading relationship between broad money growth and underlying core inflation, albeit with a variable lead time influenced particularly by exchange rate movements – chart 3. The surge in annual broad money growth, as measured by non-financial M4, from 3.6% at end-2019 to a likely peak of 16.1% in February suggests further upward pressure on the underlying core rate in 2021 -22 – the assumption here is that it will rise to 2.1% by December.

Chart 3

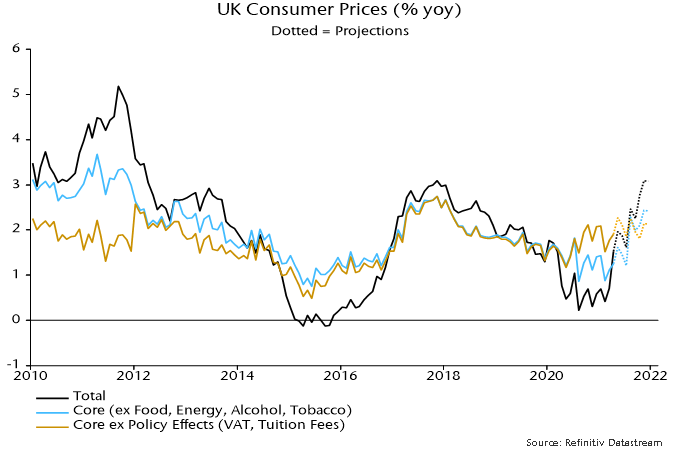

Chart 4 shows forecasts for headline, core and underlying core CPI Inflation through end-2021 based on the above assumptions. The headline rate finishes the year at 3.1% – slightly lower than in the November forecast because of the Budget decision to postpone full reversal of the VAT cut until 2022.

Chart 4