Money Moves Markets

More evidence of excessive stockpiling

November 10, 2021 by Simon Ward

Global manufacturing PMI survey results for October are consistent with the base case scenario here of a progressive loss of momentum through end-Q1 2022, at least.

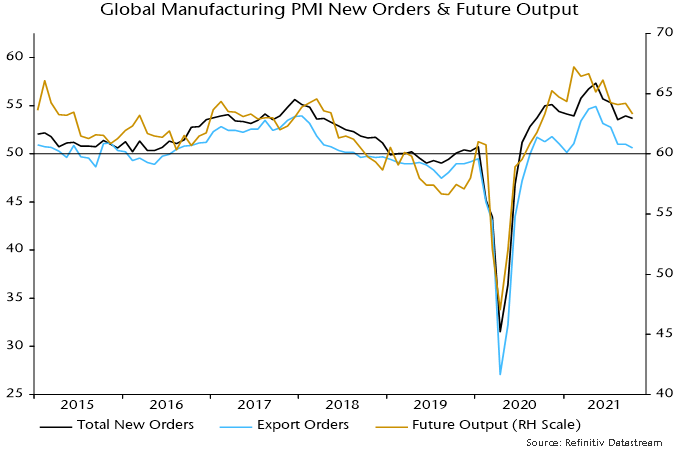

PMI new orders have moved sideways for two months but export orders and output expectations fell further last month, to nine- and 12-month lows respectively – see chart 1.

Chart 1

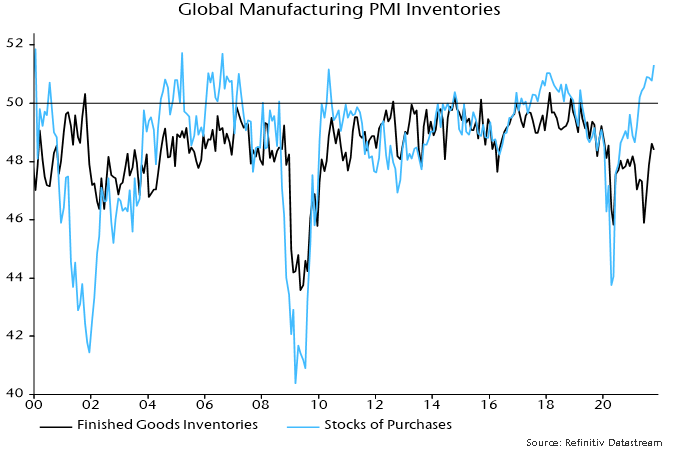

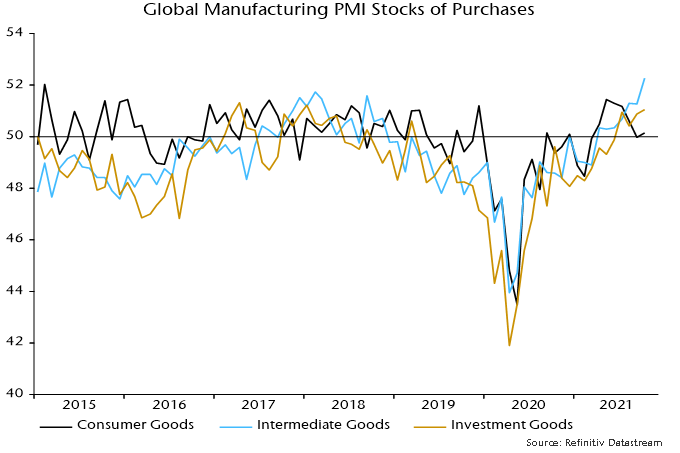

A striking feature of the survey was a further rise in the stocks of purchases index to a 15-year high – chart 2. Stockpiling of raw materials and intermediate (semi-finished) goods has been supporting new orders for producers of these inputs but the boost will fade even if stockbuilding continues at its recent pace, which is very unlikely. This is because output / orders growth is related to the rate of change of stockbuilding rather than its level.

Chart 2

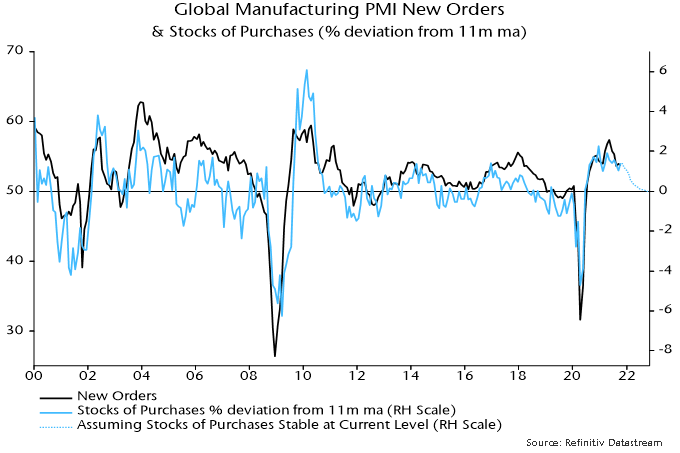

Chart 3 illustrates the relationship between new orders and the rate of change of the stocks of purchases index, with the coming drag effect expected to be greater than shown because of the high probability that stockpiling will moderate.

Chart 3

Stockbuilding of inputs has been particularly intense in the intermediate goods sector – chart 4. This suggests that upstream producers – particularly suppliers of raw materials – are most at risk from relapse in orders. Commodity prices could correct sharply as orders deflate – see also previous post.

Chart 4

A similar dynamic is playing out in the US ISM manufacturing survey, where new orders fell last month despite the inventories index reaching its highest level since 1984, resulting in a sharp drop in the orders / inventories differential – chart 5. The survey commentary attributes the inventories surge to “companies stocking more raw materials in hopes of avoiding production shortages, as well as growth in work-in-process and finished goods inventories”.

Chart 5

The combination of an ISM supplier deliveries index (measuring delivery delays) of above 70 with new orders in the 50-60 range has occurred only four times in the history of the survey. New orders fell below 50 within a year in every case.

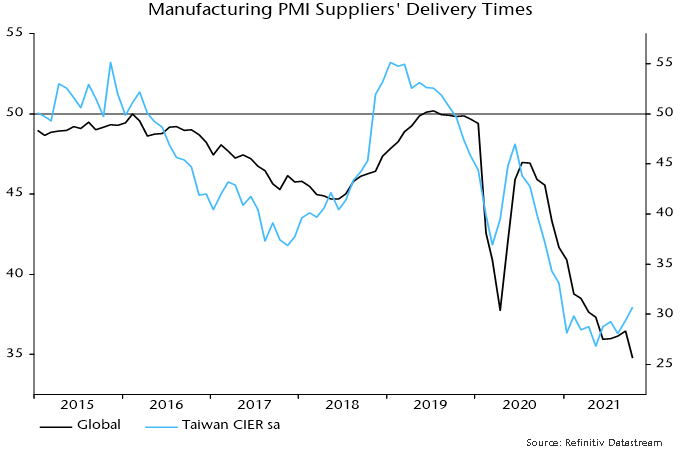

The global PMI delivery times index (which has an opposite definition to the ISM supplier deliveries index, so a fall indicates longer delays) reached a new low in October but a recent turnaround in Taiwan, which often leads, hints at imminent relief – chart 6. The view here is that current supply shortages reflect the intensity of the stockbuilding cycle upswing, with both now peaking.

Chart 6